In the technological landscape of 2026, the semiconductor industry is undergoing an unprecedented phase transition. While the 2021-2023 period was characterized by the automotive supply chain crisis, the current paradigm sees a massive redirection of capital and manufacturing capacity toward Data Center infrastructure.

This shift is not just a matter of volume, but of a technological and financial divergence that is redefining R&D roadmaps globally.

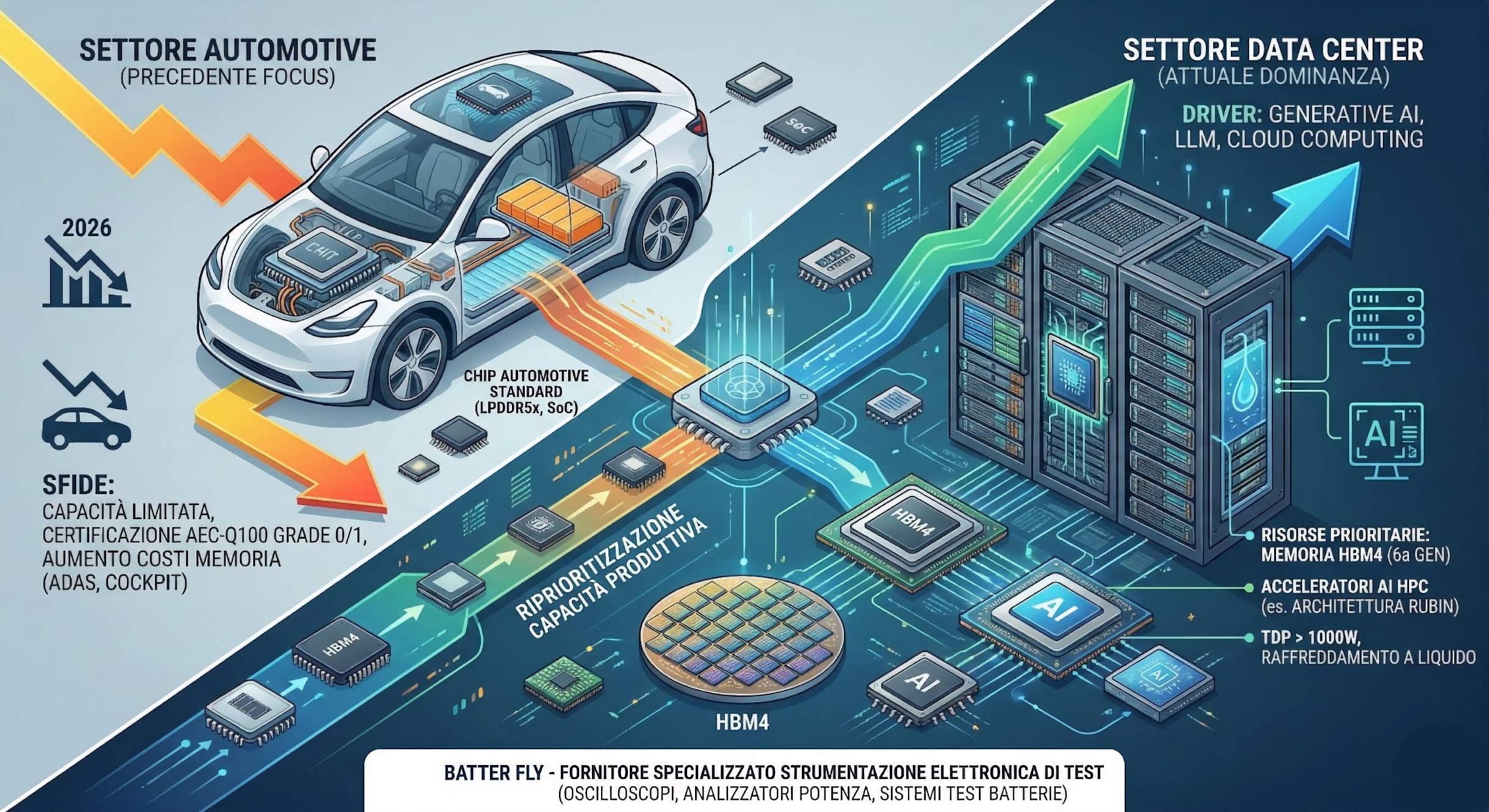

1. Capacity Erosion: HBM4 and the "Crowding-Out Effect"

The primary driver of this shift is the explosion of Generative AI, which in 2026 is expected to generate approximately 50% of the total revenue for the entire chip sector. The most critical phenomenon for system engineers is the allocation of high-performance memory.

- HBM Dominance: The production of HBM4 (6th Gen High Bandwidth Memory), essential for new AI accelerators (such as NVIDIA's Rubin architecture), is absorbing over 70% of the DRAM wafer capacity from giants like SK Hynix and Samsung.

- Automotive Impact: This causes a "crowding-out" effect for standard memories (LPDDR5x) used in ADAS control units and digital cockpits, with lead times exceeding 40 weeks again and an estimated BOM cost increase between 70% and 100%.

2. Architectural Divergence: High-Performance Computing (HPC) vs. AEC-Q100

While automotive Product Managers push toward Software-Defined Vehicles (SDV), they face limited availability of advanced nodes (<5nm) certified for the sector.

- Thermal Design Power (TDP): In data centers, we are seeing chips with TDP exceeding 1,000W (e.g., NVIDIA B200/B300), making liquid-to-liquid cooling a design standard.

- Reliability vs. Performance: Foundries prefer to optimize processes for massive computation rather than for the rigid thermal stress cycles required by AEC-Q100 Grade 0/1 standards (-40°C to +150°C). This is leading many chip manufacturers to deprioritize automotive-grade variants of their most powerful SoCs.

3. Validation and Testing Challenges for 2026

For R&D engineers, this transition introduces new complexities into validation cycles:

- Vertical Integration: Cloud Service Providers (CSPs) are developing custom ASICs internally, requiring highly specific test benches for proprietary protocols.

- Power Integrity: With increasingly lower core voltages and extremely high currents, measuring ripple and dynamic stability requires instrumentation with an extremely low noise floor and high bandwidth.

- Safety and Redundancy: The automotive sector seeks to borrow "zonal" architecture from data centers but must ensure deterministic reliability that server systems do not always offer.

Conclusions: Navigating the Change

The 2026 semiconductor market rewards computational speed and energy efficiency for the cloud. For companies operating in this scenario — whether designing next-generation AI servers or integrating advanced SDV systems — precision in the characterization and debugging phase is the critical success factor in reducing Time-to-Market.

Technical Support and Instrumentation

In such a technically complex context, the choice of a technological partner for validation is fundamental. Batter Fly confirms its role as the specialized reference supplier for electronic test instrumentation, offering cutting-edge solutions (high-resolution oscilloscopes, precision power analyzers, and battery/power test systems) indispensable for supporting R&D departments in the challenges posed by new semiconductor standards.

Leave a Comment